Break-even analysis aloud

In modern conditions of brutal competitivestruggle in the sales market is very actual is the trend of carrying out breakeven analysis on each business entity. Today, breakeven analysis of the enterprise is a very important management mechanism. It serves to correctly assess the financial situation that has developed in the enterprise. It includes measures to monitor the dynamics of financial indicators and to develop a set of measures aimed at the development of the company. In other words, in our time, breakeven analysis is the most necessary condition and the main driving force in the economic development of an industrial enterprise. On its basis, an economic strategy of stability and growth is developed, which allows to successfully exist both in the domestic and foreign markets.

In its practice, breakeven analysis is basedfor short-term resource planning. It is a study, analysis and planning of the acquisition of each unit of resources. This is done in order to know the potential benefits. And in the future - to produce and sell more products of its own production.

The activity of an industrial enterprise withoutformation of profit and loss is called break-even. The received proceeds at this type of management first goes to cover all the necessary costs, and only then each unit of the sold products brings profit. The definition of the difference between all sold products and breakeven volume is called the profit zone. The higher the profit zone at the enterprise, the stronger its financial position.

To study the dependence of the influence of the volume of production, the amount of fixed costs, the sum of the variable costs of obtaining profit, and came up with an analysis of the break-even production.

is he is very necessary and appropriate not only for the correct management of the company's financial resources, but also:

-in modernization of production facilities or in the creation of a new enterprise;

- for the development of marketing strategies in the field of price policy;

-to develop new solutions related to the introduction of a new commercial product into existing production or the removal of an old product from the production process line;

-if the output volume is changed;

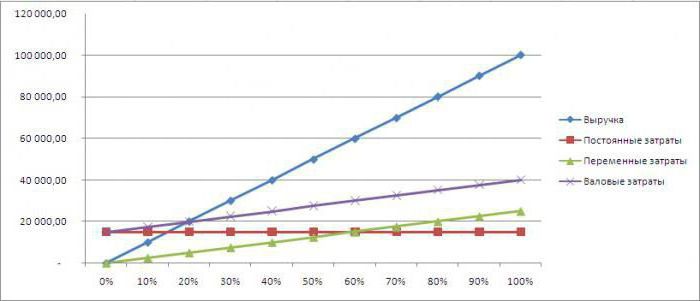

The main aspect of breakeven analysis isdefinition of the equilibrium point. In other words, this is the finding of such a volume of sales, in which the sales proceeds will be equal to the sum of all the costs incurred. The increase in this volume of sales will bring further profit, and a decrease - will lead to losses and financial collapse.

The analysis of the break-even of the enterprise includes several stages

-The first stage evaluates and studies the strongand the weak points of the business entity in terms of foreign and domestic policy. Minimized all possible costs, depending on the technical, production equipment and personnel. The activity of competitors is analyzed, the percentage share of the sales market controlled by the enterprise. The preferences of consumers and other various components are taken into account.

-On the second stage, a probable forecast is made about theThe influence of the changed prices on the cost factor of the output. The dynamics of statistical indicators for the last period is considered. Measures are discussed with unfavorable price changes.

- At the third stage, the cost is calculatedmanufactured products. The amount of work in progress is planned. All fixed and variable costs are considered. The demand and the planned volume of production in current and fixed assets are determined. The relevant financial investments are planned.

-The fourth stage determines the pointbreak-even. Moreover, in the organization of the production process, implying the production of several types of products, different prices for the nomenclature, different variable costs and a different share of the possibility of covering a mixed amount of costs are necessarily taken into account.

-On the fifth, final stage, the final preparation of the financial plan takes place taking into account the changed prices and the volume of production calculated on the basis of the breakeven point.